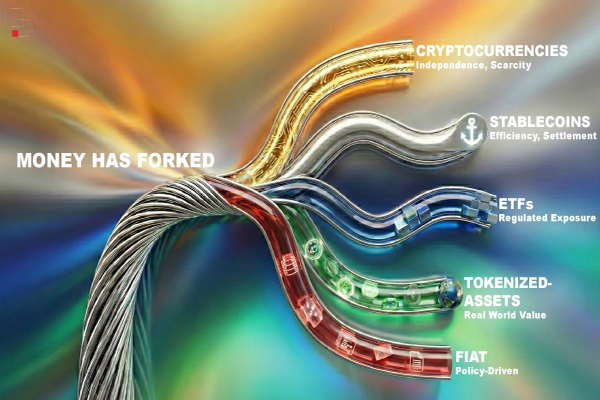

Digital money has split in two.

For more than a decade, “crypto” served as a catch-all term for everything built on blockchain technology, a volatile frontier associated with speculation, decentralization, disruption, and innovation. In 2026, that simplification no longer works. Regulation has drawn sharper boundaries, institutional adoption has formalized categories, and practical utility has separated from ideology. The digital asset ecosystem, now valued at roughly $2.3 trillion, is no longer a single experiment but two parallel monetary systems evolving side by side. Stablecoins account for more than $310 billion in circulating supply and are expanding faster than volatile crypto assets on a relative basis. In 2025 alone, stablecoin transaction volume reached approximately $33 trillion, rivaling the throughput of major traditional payment networks. That figure is not a trading statistic; it is an infrastructure milestone. The divide is philosophical as well as economic. On one side are unbound assets, cryptocurrencies such as Bitcoin and Ethereum, whose value is shaped entirely by market forces, scarcity, network effects, and collective belief. On the other are anchored instruments, stablecoins engineered to maintain a fixed value, typically backed one to one by cash and short term government securities. Cryptocurrencies represent monetary independence, while stablecoins represent monetary efficiency.

The Unbound System: Digital Commodities

Bitcoin introduced programmable scarcity through its fixed 21 million coin supply, positioning itself as a hedge against monetary expansion and systemic risk. Over time, it matured into institutional “digital gold,” reinforced by spot ETFs, corporate treasury allocations, and even sovereign participation. Ethereum expanded this foundation by embedding programmability directly into money, enabling decentralized exchanges, lending protocols, tokenized assets, and on-chain governance systems. These networks are not merely digital currencies; they function as parallel financial infrastructures.

Yet volatility remains a defining characteristic. Even in 2026, double-digit monthly price swings are common. While open market price discovery creates the potential for asymmetric upside, it also makes these assets impractical for payroll, trade settlement, treasury management, or automated financial workflows. Cryptocurrencies are therefore optimized for capital appreciation, governance participation, and macro exposure. They are assets primarily meant to be held, not spent.

The Anchored System: Digital Cash

Stablecoins were built for a fundamentally different objective than cryptocurrencies. They are not designed to appreciate in value but to maintain stability. Their purpose is simple: bring fiat currency onto blockchain rails without sacrificing speed, transparency, or programmability. When properly structured, each stablecoin represents a redeemable claim on high quality reserves such as cash or short term government securities. Its value is anchored not in market sentiment or scarcity, but in verifiable backing.

In their early years, stablecoins were often dismissed as mere trading tools, temporary parking spots that allowed investors to move between volatile positions without returning to the banking system. That perception no longer reflects reality. Today, stablecoins form the settlement foundation of the digital asset ecosystem. More than 70 percent of decentralized exchange liquidity is denominated in dollar pegged tokens, and lending markets depend on them as stable collateral. During periods of market stress, capital frequently rotates into stablecoins rather than leaving the ecosystem altogether, preserving liquidity and enabling rapid redeployment.

Stablecoins are not rivals to cryptocurrencies. They are the infrastructure that makes cryptocurrency markets function efficiently.

Speculation vs. Settlement

The fundamental divide in 2026 is velocity. Cryptocurrencies are designed to accumulate value over time, while stablecoins are engineered to circulate value efficiently. This distinction has reshaped market structure. Across both centralized and decentralized exchanges, fiat typically serves as the entry and exit point, stablecoins act as the base settlement currency, and cryptocurrencies represent the traded assets layered on top. In decentralized finance, stablecoins anchor liquidity pools, reduce slippage, and provide the pricing stability necessary for swaps, lending, and arbitrage.

Their advantage becomes even more pronounced in cross-border commerce. Traditional international transfers often rely on multiple correspondent banks, operate within limited business hours, take two to five days to settle, and include opaque foreign exchange spreads. Stablecoin transfers, by contrast, settle in minutes, operate continuously, require minimal intermediaries, and provide transparent, on-chain reconciliation. For this reason, stablecoins are increasingly used for remittances, corporate treasury management, exchange settlement, and tokenized asset delivery-versus-payment transactions. They have evolved into a geographically neutral, always-on global settlement currency.

Regulation Draws a Line

The decoupling between anchored and unbound assets is reinforced by law. In the United States, structured stablecoin legislation has advanced significantly, creating a clearer legal distinction between regulated payment stablecoins and market-driven crypto assets. Europe’s MiCA framework is fully operational.

For the first time, regulation explicitly differentiates:

| Dimension | Regulated Stablecoins | Cryptocurrencies |

| Legal classification | Payment instrument | Digital commodity or security |

| Backing | 1:1 reserves (cash, short-term Treasuries) | Market-driven |

| Primary role | Settlement & payments | Store of value & network utility |

| Volatility | Pegged | Market-based |

This clarity has accelerated institutional entry. Banks and infrastructure providers are launching permitted payment stablecoins not as speculative products, but as regulated settlement rails.

Stablecoins are increasingly treated as financial infrastructure.

Stablecoins vs ETFs: Exposure vs Utility

As institutional participation expands, a new comparison has entered the conversation: stablecoins versus ETFs. Although they may coexist within the same digital asset ecosystem, their purposes are fundamentally different. ETFs are designed to provide regulated price exposure to an underlying asset, allowing investors to participate in its performance without directly holding it. Stablecoins, by contrast, are built for monetary utility. They function as programmable digital cash that can move instantly and settle transactions in real time. An ETF cannot pay a supplier, settle a cross-border invoice, or execute an automated micro-payment. A stablecoin can. This distinction highlights the layered architecture of modern digital finance: cryptocurrencies operate as programmable commodities, ETFs deliver regulated investment exposure, and stablecoins serve as the settlement layer that enables value to move.

| Dimension | Stablecoins | ETFs |

| Legal form | Digital token | Regulated investment fund |

| Trading hours | 24/7 | Market hours |

| Settlement | Near-instant | T+1 / T+2 |

| Redemption | Direct with issuer | Authorized participants |

| Usable as money | Yes | No |

Tokenized Value: Gold and Treasuries

Between the anchored and unbound systems lies an emerging category: tokenized real world assets. Gold backed tokens represent direct claims on physical bullion and function as digital commodity money, while treasury backed tokens offer yield and stability, operating more like digital cash equivalents than speculative instruments. These assets blur traditional financial boundaries and demonstrate that tokenization is not confined to volatility or price discovery. It can embed stability, income, and real world value directly into programmable digital form. Rather than converging into a single model, the ecosystem is broadening across multiple layers of financial utility.

The AI Economy and Machine-Native Money

A defining shift in 2026 is the rise of machine-executed commerce. Autonomous AI systems are increasingly managing API purchases, subscription payments, compute resources, and micro-contracts in real time. These systems require programmable and deterministic money that behaves predictably within automated workflows. Traditional payment methods such as credit cards settle slowly and depend on intermediaries, while volatile crypto assets can introduce budget instability during execution. Stablecoins offer immediate settlement, fractional precision, and consistent dollar-denominated value. In a machine-native economy, stability is not a conservative choice; it is an operational requirement.

The Broader Monetary Landscape

Central bank digital currencies add another dimension to the evolving monetary landscape. China’s digital yuan is already operational at scale, Europe continues advancing its digital euro pilot, and the United States remains in active policy debate. While CBDCs may ultimately dominate domestic wholesale settlement systems, private stablecoins continue to lead global cross border usage. For now, stablecoins remain the most widely adopted programmable settlement layer internationally.

As this evolution unfolds, the digital monetary system is taking on a layered structure. Stablecoins operate as the transaction and liquidity layer. Cryptocurrencies function as the value and governance layer. Tokenized real world assets introduce yield bearing instruments. Smart contracts automate execution, and AI systems increasingly interact with these rails autonomously. The market is no longer a monolith. It has become a structured financial stack.

Risk, Maturity, and Complementarity

Neither side is risk free. Cryptocurrencies remain exposed to cyclical drawdowns, shifting liquidity conditions, and evolving regulatory frameworks. Stablecoins face their own challenges, including reserve transparency scrutiny, potential depeg events, and concentration risk among major issuers. The distinction is not that one is safe and the other is risky, but that they carry fundamentally different types of risk.

A mature financial ecosystem requires both volatility and stability. Innovation depends on risk capital and open price discovery, while commerce depends on predictable settlement and monetary consistency. Cryptocurrencies are primarily held by investors seeking macro exposure and participation in decentralized networks. Stablecoins, by contrast, are deployed as transactional instruments to move value, settle obligations, and automate financial activity.

Money Has Forked

Digital money did not converge into a single form. It matured into complementary systems, each designed to solve a different economic problem. Cryptocurrencies embody monetary independence and programmable scarcity. Stablecoins deliver efficiency, settlement certainty, and institutional integration. ETFs provide regulated investment exposure, while tokenized assets bring real world value onto digital rails.

Exposure is not utility. Volatility is not settlement. A functioning programmable financial system requires both anchored stability and unbound price discovery.

The real competition is not between stablecoins and cryptocurrencies. It is between programmable finance and legacy infrastructure. In 2026, anchored and unbound systems are no longer confused for one another. They are advancing in parallel, reshaping how value moves across borders, across machines, and across markets.

Digital finance is no longer a speculative experiment. It is an architectural transition. Those who understand which instruments are meant to be held and which are meant to be used will not just survive this shift. They will help define it.

Refer: Pavna Jain post here.